Navigation auf uzh.ch

Navigation auf uzh.ch

By Stefano Battiston (UZH) and Irene Monasterolo (WU Vienna).

How green or brown is the European Central Bank’s (ECB) Quantitative Easing (QE)? How could it support the EU in achieving its 2030 energy transition targets?

This question has been asked (Barkawi 2017; Matikainnen ea. 2017; Monnin 2018; Schoenmaker 2019) since the beginning of the QE and in particular in relation to the purchase of corporate bonds, i.e. the Corporate Sector Purchase Program (CSPP), implemented by six National Central Banks (NCBs). In order to advance the discussion further, we construct a bond market Benchmark that mimics the CSPP eligibility criteria and analyse its exposure to economic sectors that are relevant for climate policies and for the energy transition. In this blog, we will post dashboards with results from our ongoing work and collect comments to inform the discussion.

Follow us on Twitter Stefano Battiston @zbattiz, Irene Monasterolo @Transitionway

Press coverage: March 21st article on Le Monde

Current version of the report (PDF, 1 MB)

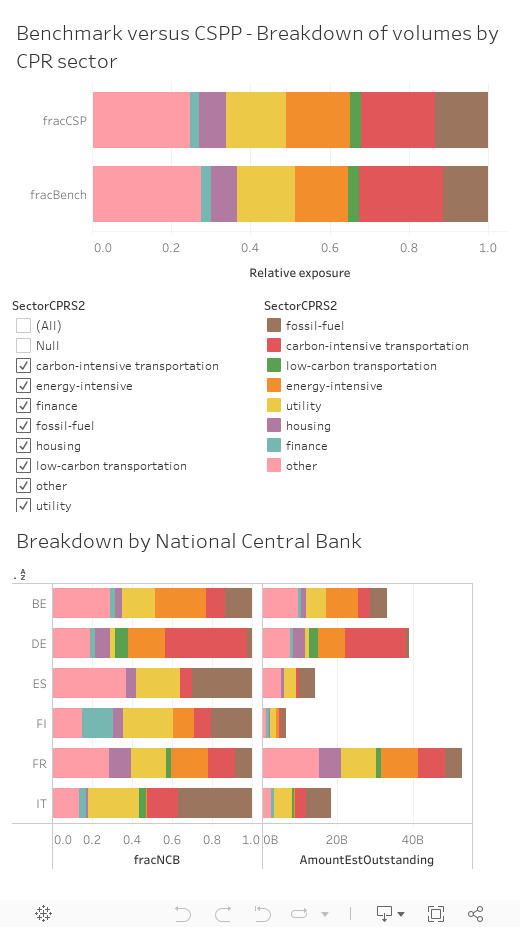

Captions. The first infographic shows the composition by relative volume and sector of the corporate bonds in the Benchmark and in the CSPP. The composition of the CSPP is very close to the market Benchmark. However, under several criteria the market benchmark is not aligned to the EU targets for the energy transition. See more in the paper and upcoming infographics on this blog. The second infographic shows the same breakdown for each of the six National Central Banks tasked with the CSPP. Notice the differences in volumes across sectors and countries. NOTE: hovering over the bottom left bar char shows detail of individual issuers.

Methods. The NACE sectors have been grouped into Climate Policy Relevant Sectors (see Methodology in the paper):

Background. In the discussion on greening the financial system (see NGFS) and promoting climate-related financial disclosure (see the TCFD work), there has been a growing attention on the European Central Bank’s Quantitative Easing Corporate Sector Purchase Program (CSPP) implemented by six National Central Banks (NCBs). In particular, it has been argued that the CSPP might imply a bias towards carbon intensive sectors (Barkawi 2017; Matikainnen ea. 2017; Monnin 2018; Schoenmaker 2019). Previous analyses did not develop a benchmark against which compare the CSPP sectors’ composition. This step is allows to make more precise statements about the alignment of the European market and ECB’s monetary policy to sustainability, beyond the CSPP. Nevertheless, building the benchmark is not trivial. Indeed, ECB’s eligibility criteria sometimes leave space for interpretation at the level of individual firm (e.g. in the finance sector), and because the ECB doesn’t publish the amount effectively purchased by each NCB.

Preliminary Results. We construct a benchmark composed of 1557 securities issued by 282 firms, and a CSPP universe composed of 1097 securities issued by 237 firms. We compare the exposures to carbon-intensive sectors (reclassified into Climate Policy Relevant Sectors) of the benchmark, the CSPP and the individual NCB’s purchases, at the level of individual security and issuer. Our results show that the CSPP closely follows the benchmark, which is mostly composed of issuances from fossil fuel and carbon-intensive companies associated to long-term maturities. In contrast, green bonds’ share is still residual, despite green bonds being issued also by carbon-intensive companies. In addition, the exposure to the most carbon-intensive sectors is very heterogeneous across NCBs, with Banca d’Italia and the Bundesbank being respectively most exposed to fossil and automotive companies.

Insights for discussion. Thus, in order to effectively support the sustainable finance transition without prejudice on its market neutrality, in the further steps of its CSPP, the ECB might want to introduce a weight for carbon-intensive companies that are diversifying their portfolio towards low-carbon investments (e.g. in the utility, transport, automotive sectors). This would also contribute to decrease the exposure of the Euro Area financial market and real economy to the risk of carbon stranded assets, thus preventing the onset of price volatility and financial instability. However, this would imply to consider the “shades of brown” (i.e. a negative discrimination) of economic activities in the design of the European Commission’s green taxonomy.

Keywords: Central banks, Quantitative Easing, corporate bonds’ market, carbon-intensity, benchmark, green bonds.

Aknowledgments: This study has been prepared for Institut Veblen and Positive Money Europe.

References (see full list in the report)

Monnin, P. (2018) Central Banks and the Transition to a Low-Carbon Economy, CEP Discussion Note.

Schoenmaker, D., 2019. Greening monetary policy. CEPR working paper, available at SSRN 3242814.