Navigation auf uzh.ch

Navigation auf uzh.ch

What are the effects on financial stability of the interplay between climate policy shocks and market conditions?

To answer this question we combine the frameworks of the Climate Stress-test with the framework of the network valuation of financial assets and common asset contagion involving not only banks but also investment funds.

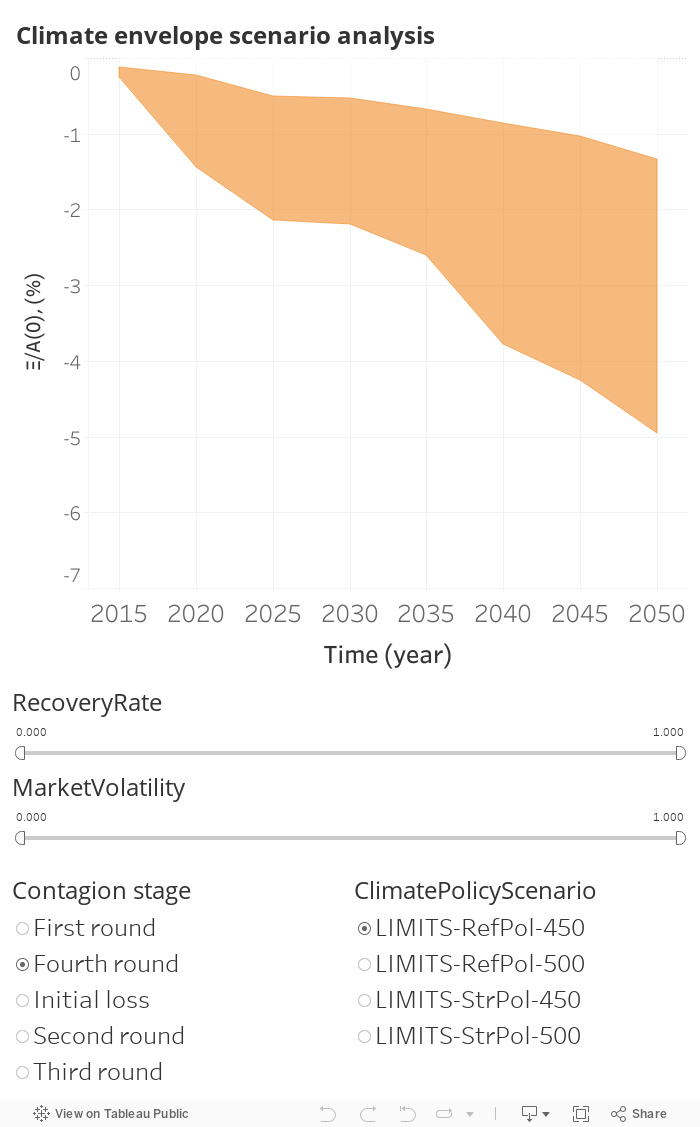

Captions. The infographic illustrates the climate envelope scenario analysis, i.e. the losses (as a percentage of initial total assets) suffered by the mexican financial. The x-axis represent the year of the disorderly transition towards climate targets. The y-axis represents the relative shock suffered by financial institutions. With filters, the user is able to select among the four different climate policy scenarios, as well as to set the range for the market conditions (recovery rate and market volatility). Further, it is possible to observe the losses in the five stages of the contagion dynamics: 1) initial losses on the asset classes, 2) the losses due to direct exposures (first round), 3) the losses due to direct contagion in the interbank network (second round), 4) the losses due to indirect contagion (third round, asset firesales), and 5) the losses that are too large to be absorbed by banks' capital and are thus transferred to external creditors (fourth round). Notice that stages are cumulative (i.e. fourth round includes third round).

The extended bank-fund climate stress test. In this paper we extend the models of financial contagion to derive the first climate stress-test methodology that combines an ex-ante valuation of financial assets, an endogenous recovery rate and a fire-sales reaction that consider several types of financial institutions at the same time. The dynamics of contagion can be summarized as follows:

Policy implications. Our results have three main policy implications.

Keywords: financial stability, climate risk, sustainable finance, climate stress-test, low-carbon transition risk, 2°C opportunities.